![]()

Notebook: Discrete Time#

Shock elasticities quantify the (local) exposures of macroeconomic cash flows to shocks over alternative investment horizons and the corresponding prices or investors’ compensations. Here we cover shock elasticities for models that are exponential-quadratic. This model structure is particularly tractable with quasi-analytical solutions. This notebook implements methods and formulas developed in [2] and [3].

Section 1 introduces the exponential–quadratic framework. It supposes this structure emerges as an approximation with the approximation taken as input into the computer code.

Section 2 presents shock elasticity formulas for both exposure and price elasticities.

Section 3 provides an illustration using the long-run risk model [1].

This notebook provides both written explanations and accompanying code. The simplest way to run the code is to open the Google Colab link at the top of this page. Otherwise, the reader can copy the code snippets onto their local machine.

1. Exponential-linear-quadratic Framework#

We suppose a linear-quadratic specification of the state dynamics:

The code will take the coefficients as inputs.

One way to construct such a system is to consider a family of the dynamic systems

parameterized by \(\sf q\). We calculate a second-order approximation of stochastic processes around the ``small noise’’ limit \({\sf q} = 0\):

where \(X_{t}^m\) is the date \(t\), \(m^{th}\)-order derivatitve approximation. This gives a version of the system where

and \(\psi_i\) is the derivative of \(\psi\) with respect to argument \(i\) evaluated at \((\bar x, 0, 0)\). There are analogous formulas for the remaining matrices.

For the purposes of the code we take the dynamic state evolution as a starting point with state vector

as the Markov state with evolution.

We suppose that the logarithms of macroeconomic and stochastic discount factor processes that interest us grow or decay stochastically over time with stationary increments. Let \(Y\) be the logarithm of such a process. The process \(Y\) will display linear growth or decay. We refer to its exponential \(M = \exp(Y)\) as a multiplicative process. We use multiplicative processes to capture growth or decay in levels. We presume that

Again we could derive this by embedding the \(Y\) process in a parameterized family of processes with increments given by

We approximate the resulting processes as:

Following the steps of our approximation of \(X\), we write

where \(\kappa_i\) is the derivative of \(\kappa\) with respect to argument \(i\) evaluated at \((\bar x, 0, 0)\) and similarly for the second derivatives. We set \({\sf q} = 1\).

In what follows, \(M\) will be a macro growth process, a stochastic discount factor process, or a product of the two. The user inputs are the quadratic specifications in equation (1) and equation (2).

import os

import sys

workdir = os.getcwd()

# !git clone https://github.com/lphansen/RiskUncertaintyValue # Please uncomment this line when running on the google colab

# workdir = os.getcwd() + '/RiskUncertaintyValue' # Please uncomment this line when running on the google colab

sys.path.insert(0, workdir+'/src')

from IPython.display import display, HTML

display(HTML("<style>.container { width:97% !important; }</style>"))

import numpy as np

np.set_printoptions(suppress=True)

from scipy.stats import norm

from numba import njit, prange

from lin_quad import LinQuadVar

from lin_quad_util import next_period, log_E_exp, kron_prod, distance

from utilities import mat, vec, sym

from elasticity import exposure_elasticity, price_elasticity

"""

Python object 'LinQuadVar' stores the coefficients of a variable that has the linear-quadratic structure as shown in equations (1) and (2).

Below is an example of constructing a variable using the 'LinQuadVar'.

"""

n_Y = 1 # The dimension of the LinQuadVar, here we construct a one dimensional (scalar) LinQuadVar

n_X = 2 # The dimension of state variables, X_t

n_W = 4 # The dimension of shocks, W_t

lq = LinQuadVar({'c': np.array([[0.0015]]), # The constant term

'x': np.array([[1., 0.]]), # The coefficients on X_{1,t}

'w': np.array([[0., 0., 0.0078, 0. ]]), # The coefficients on W_{t+1}

'x2': np.array([[0.5, 0.]]), # The coefficients on X_{2,t}

'xw': np.array([[0., 0., 0., 0., 0., 0., 0.0039, 0.]])}, # The coefficients on X_{1, t} \otimes W_{t+1}

shape = (n_Y, n_X, n_W)) # The dimensions of LinQuadVar, X_t, and, W_t

## Display the coefficients of the LinQuadVar

lq.coeffs

---------------------------------------------------------------------------

ModuleNotFoundError Traceback (most recent call last)

/var/folders/w8/yzmpdfnn56n_rrj09q0r6spc0000gn/T/ipykernel_36887/3935067666.py in <module>

12 from numba import njit, prange

13

---> 14 from lin_quad import LinQuadVar

15 from lin_quad_util import next_period, log_E_exp, kron_prod, distance

16 from utilities import mat, vec, sym

ModuleNotFoundError: No module named 'lin_quad'

2. Shock Elasticity#

2.1 Analytical framework#

Shock elasticities are used to quantify the date \(t\) impact on values of exposure to the shock \( (\alpha_0 + \alpha_1 X_0) \cdot W_1\) at date one. It has the form shown in equation 3:

Using the linear-quadratic dynamics of section 1, the computer software computes the logarithm of the denominator of formula (3):

recursively. Form

Conveniently, we can express the outcomes as:

for some specification of \({\widetilde \Phi}_i\), \(i=0,1,2,3\). In words, the \({\mathbb M}\) operator maps linear-quadratic functions into linear-quadratic functions. The code uses this mapping repeatedly.

By a direct application of the Law of Iterated Expectations we have that

where \({\mathbb M}^{t-1}[1]\) means to apply the operator \({\mathbb M}\) \(t-1\) times in succession to a function that is identically one. Observe that \({\mathbb M}^{t-1}[1]\) is a function of \(x\).

The function _Φ_star defined below calculates the linear-quadratic dynamic coefficients in \(\mathbb{M}\) mappings and iterations.

To complete the calculation of the elasticity, note that

This leads us to construct the nonegative random variable:

Notice that \(L_{t}\) depends only date one information and has expectation one conditioned on date zero information. Multiplying this positive random variable by \(W_1\) and taking expectations is equivalent to changing the conditional probability distribution and evaluating the conditional expectation of \(W_1\) under this change of measure. Since \(W_1\) is normally distributed, the exponential quadratic construction of \(L_{t}\) implies that \(W_1\) remains normally distributed but with a different mean and covariance matrix. The computer codes use this observation to evaluate formula (5) by taking an altered conditional expectation of \(W_1\). The derivation details to compute the conditional moments under the change of probability measure implied by \(L_t\) can be found in [2], Appendix B, and [3], Appendix A.

For the purposes of the code, denote the conditional mean induced by \(L_{t}\) as \(\mu_{t}^0 + \mu_{t}^1 x_1\) and the conditional covariance matrix \({\widetilde \Sigma}_t\).

def _Φ_star(log_M_growth, X1_tp1, X2_tp1, T):

r"""

Computes :math:`\Phi^*_{0,t-1}`, :math:`\Phi^*_{1,t-1}`, :math:`\Phi^*_{2,t-1}`, :math:`\Phi^*_{3,t-1}` in equation (4).

Parameters

----------

log_M_growth : LinQuadVar

Log growth of multiplicative functional M.

e.g. log consumption growth, :math:`\log \frac{C_{t+1}}{C_t}`

X1_tp1 : LinQuadVar

Stores the coefficients of laws of motion for X1.

X2_tp2 : LinQuadVar or None

Stores the coefficients of laws of motion for X2.

T : int

Time horizon.

Returns

-------

Φ_star_1tm1_all : (T, 1, n_X) ndarray

Φ_star_2tm1_all : (T, 1, n_X) ndarray

Φ_star_3tm1_all : (T, 1, n_X**2) ndarray

"""

_, n_X, _ = X1_tp1.shape

Φ_star_1tm1_all = np.zeros((T, 1, n_X))

Φ_star_2tm1_all = np.zeros((T, 1, n_X))

Φ_star_3tm1_all = np.zeros((T, 1, n_X**2))

log_M_growth_distort = log_E_exp(log_M_growth)

X1X1 = kron_prod(X1_tp1, X1_tp1)

for i in range(1, T):

Φ_star_1tm1_all[i] = log_M_growth_distort['x']

Φ_star_2tm1_all[i] = log_M_growth_distort['x2']

Φ_star_3tm1_all[i] = log_M_growth_distort['xx']

temp = next_period(log_M_growth_distort, X1_tp1, X2_tp1, X1X1)

log_M_growth_distort = log_E_exp(log_M_growth + temp)

return Φ_star_1tm1_all, Φ_star_2tm1_all, Φ_star_3tm1_all

2.2 Limiting Behavior#

The operator \({\mathbb M}\) typically has a solution to the following equation:

The solution of interest when, it exists, can be deduced by iterating on the \({\mathbb M}\) operator allowing for a constant shift \(\eta^e\). This solution gives a characterization of the limiting elasticity. Construct

The elasticities are given by conditional linear combinations of conditional expectations of \(W_1\) under this limiting change of measure.

To express the equation of interest differently, consider the operator, \({\mathbb P}\) that maps \(\Phi_{0} +\Phi_1 x_1+\Phi_2 x_2 + {\frac 1 2} (x_1)'\Phi_3 x_1\) into \(\exp\left({\mathbb M} \left[ \Phi_{0} +\Phi_1^e x_1+\Phi_2 x_2 + {\frac 1 2} (x_1)'\Phi_3 x_1\right] \right)\). Rewrite equation (6) as:

which is an eigenvalue equation where \(\exp\left[ \Phi_1^e x_1+\Phi_2^e x_2 + {\frac 1 2} (x_1)'\Phi_3^e x_1\right]\) is a postive eigenfunction and \(\exp(\eta)\) is a positive eigenvalue. [1]

The codes below solve the eigenvalue problem using the M_mapping.

def M_mapping(log_M_growth, f, X1_tp1, X2_tp1, second_order = True):

r'''

Computes coefficients of a LinQuadVar after one iteration of M mapping

Parameters

----------

log_M_growth : LinQuadVar

Log difference of multiplicative functional.

e.g. log consumption growth, :math:`\log \frac{C_{t+1}}{C_t}`

f : LinQuadVar

The function M Mapping operate on.

e.g. A function that is identically one, log_f = LinQuadVar({'c': np.zeros((1,1))}, log_M_growth.shape)

X1_tp1 : LinQuadVar

Stores the coefficients of laws of motion for X1.

X2_tp2 : LinQuadVar or None

Stores the coefficients of laws of motion for X2.

second_order: boolean

Whether the second order expansion of the state evoluton equation has been input

Returns

-------

LinQuadVar, stores the coefficients of the new LinQuadVar after one iteration of M Mapping

'''

if second_order:

return log_E_exp(log_M_growth + next_period(f, X1_tp1, X2_tp1))

else:

if X2_tp1 != None:

print('The second order expansion for law of motion is not used in the first order expansion.')

return log_E_exp(log_M_growth + next_period(f, X1_tp1))

def Q_mapping(log_M_growth, f, X1_tp1, X2_tp1, tol = 1e-10, max_iter = 10000, second_order = True):

r'''

Computes limiting coefficients of a LinQuadVar by recursively applying the M mapping operator till convergence, returns the eigenvalue and eigenvector.

Parameters

----------

log_M_growth : LinQuadVar

Log difference of multiplicative functional.

e.g. log consumption growth, :math:`\log \frac{C_{t+1}}{C_t}`

f : LinQuadVar

The function M Mapping operate on.

e.g. A function that is identically one, log_f = LinQuadVar({'c': np.zeros((1,1))}, log_M_growth.shape)

X1_tp1 : LinQuadVar

Stores the coefficients of laws of motion for X1.

X2_tp2 : LinQuadVar or None

Stores the coefficients of laws of motion for X2.

tol: float

tolerance for convergence

max_iter: int

maximum iteration

second_order: boolean

Whether the second order expansion of the state evoluton equation has been input

Returns

-------

Qf_components_log : List of LinQuadVar

stores the coefficients of the LinQuadVar in each iteration of M Mapping

f: LinQuadVar

The function M Mapping operate on.

e.g. A function that is identically one, log_f = LinQuadVar({'c': np.zeros((1,1))}, log_M_growth.shape)

η: float

The eigenvalue

η_series: list of float

The convergence path of the eigenvalue

'''

η_series = []

Qf_components_log = []

for i in range(max_iter):

Qf_components_log.append(f)

if second_order:

f_next = M_mapping(log_M_growth, f, X1_tp1, X2_tp1, second_order = second_order)

else:

if X2_tp1 != None:

print('The second order expansion for law of motion is not used in the first order expansion.')

f_next = M_mapping(log_M_growth, f, X1_tp1, second_order = second_order)

η = (f_next['c'] - f['c']).item()

η_series.append(η)

if distance(f, f_next, ['x', 'xx', 'x2']) < tol:

break

f = f_next

if i >= max_iter-1:

print("Warning: Q iteration may not have converged.")

Qf_components_log.append(f_next)

return Qf_components_log, f, η, η_series

The function _elasticity_coeff defined below calculates the conditional mean induced by \(L_{t}\) as \(\mu_{0,t} + \mu_{1,t} x_1\) and the covariance matrix as \({\widetilde \Sigma}_{t}.\)

def _elasticity_coeff(log_M_growth, X1_tp1, X2_tp1, T):

r"""

Computes :math:`\mu_{t,0}`, :math:`\mu_{t,1}`, :math:`\tilde{\Sigma}_t`. Corresponding formulas can be found in [3], Jaroslav and Hansen (2014), Appendix B.

Parameters

----------

log_M_growth : LinQuadVar

Log difference of multiplicative functional.

e.g. log consumption growth, :math:`\log \frac{C_{t+1}}{C_t}`

X1_tp1 : LinQuadVar

Stores the coefficients of laws of motion for X1.

X2_tp2 : LinQuadVar or None

Stores the coefficients of laws of motion for X2.

T : int

Time horizon.

Returns

-------

Σ_tilde_t_all : (T, n_W, n_W) ndarray

μ_t0_all : (T, n_W, 1) ndarray

μ_t1_all : (T, n_W, n_X) ndarray

"""

_, n_X, n_W = log_M_growth.shape

Φ_star_1tm1_all, Φ_star_2tm1_all, Φ_star_3tm1_all = _Φ_star(log_M_growth, X1_tp1, X2_tp1, T)

Ψ_0 = log_M_growth['w']

Ψ_1 = log_M_growth['xw']

Ψ_2 = log_M_growth['ww']

Λ_10 = X1_tp1['w']

if log_M_growth.second_order:

Λ_20 = X2_tp1['w']

Λ_21 = X2_tp1['xw']

Λ_22 = X2_tp1['ww']

else:

Λ_20 = np.zeros((n_X,n_W))

Λ_21 = np.zeros((n_X,n_X*n_W))

Λ_22 = np.zeros((n_X,n_W**2))

Θ_10 = X1_tp1['c']

Θ_11 = X1_tp1['x']

Σ_tilde_t_all, μ_t0_all, μ_t1_all \

= _elasticity_coeff_inner_loop(Φ_star_1tm1_all, Φ_star_2tm1_all, Φ_star_3tm1_all, Ψ_0, Ψ_1, Ψ_2, Λ_10, Λ_20, Λ_21, Λ_22, Θ_10, Θ_11, n_X, n_W, T)

return Σ_tilde_t_all, μ_t0_all, μ_t1_all

@njit

def _elasticity_coeff_inner_loop(Φ_star_1tm1_all, Φ_star_2tm1_all, Φ_star_3tm1_all, Ψ_0, Ψ_1, Ψ_2, Λ_10, Λ_20, Λ_21, Λ_22, Θ_10, Θ_11, n_X, n_W, T):

Σ_tilde_t_all = np.zeros((T, n_W, n_W))

μ_t0_all = np.zeros((T, n_W, 1))

μ_t1_all = np.zeros((T, n_W, n_X))

kron_Λ_10_Λ_10 = np.kron(Λ_10,Λ_10)

kron_Θ_10_Λ_10_sum = np.kron(Θ_10,Λ_10) + np.kron(Λ_10,Θ_10)

temp = np.kron(Λ_10, Θ_11[:, 0:1].copy())

for j in range(1, n_X):

temp = np.hstack((temp, np.kron(Λ_10, Θ_11[:, j:j+1].copy())))

kron_Θ_11_Λ_10_term = np.kron(Θ_11, Λ_10) + temp

for t in prange(T):

Φ_star_1tm1 = Φ_star_1tm1_all[t]

Φ_star_2tm1 = Φ_star_2tm1_all[t]

Φ_star_3tm1 = Φ_star_3tm1_all[t]

Σ_tilde_t_inv = np.eye(n_W)- 2 * sym(mat(Ψ_2 + Φ_star_2tm1@Λ_22 + Φ_star_3tm1@kron_Λ_10_Λ_10, (n_W, n_W)))

μ_t0 = (Ψ_0 + Φ_star_1tm1@Λ_10 + Φ_star_2tm1@Λ_20 + Φ_star_3tm1 @ kron_Θ_10_Λ_10_sum).T

μ_t1 = mat(Ψ_1 + Φ_star_2tm1 @ Λ_21 + Φ_star_3tm1 @ kron_Θ_11_Λ_10_term,(n_W, n_X))

Σ_tilde_t_all[t] = np.linalg.inv(Σ_tilde_t_inv)

μ_t0_all[t] = μ_t0

μ_t1_all[t] = μ_t1

return Σ_tilde_t_all, μ_t0_all, μ_t1_all

2.3 Exposure and Price Elasticities#

We consider two types of multiplicative processes, one that captures macroeconomic growth, denoted by \(G\), and another that captures stochastic discounting, denoted by \(S\).

The stochastic discount factor process, \(S\), is typically computed from the underlying economic model to reflect equilibrium valuation dynamics.

For instance, the growth process \(G\) might be a consumption process or some other endogenously determined cash flow, or it might be an exogenously specified technology shock process that grows through time.

The interplay between \(S\) and \(G\) will determine uncertainty compensations over multi-period investment horizons.

Consider the pricing of a vector of payoffs \(G_tW_1\) in comparison to the scalar payoff \(G_t\).

The shock-exposure elasticity is constructed as from the ratio of expected payoffs \(E[G_tW_1 |X_0 =x]\) relative to \(E [G_t | X_0 = x]\). To calculate shock-exposure elasticity, the multiplicative functional \(M\) is set as \(G\).

\[ \varepsilon_{g}( x, t)= \frac{(\alpha_0 + \alpha_1 x) \cdot {\mathbb E}\left[\left( \frac {G_t}{G_0}\right) W_1 \mid X_0 = x\right]}{{\mathbb E} \left(\frac {G_t}{G_0} \mid X_0 = x\right)} \]This is done by the function _exposure_elasticity. This function uses the _elasticity_coeff defined in the last section.

The shock-price elasticity includes an adjustment for the values of the payoffs \(E [S_t G_t W_1 | X_0 = x]\) relative to \(E [S_t G_t | X_0 = x]\). To calculate shock-price elasticity, the multiplicative functional \(M\) is set as the product \(SG\).

The shock-price elasticity is:

This computation is done by the function price_elasticity. This function also uses the _elasticity_coeff defined in the last section.

Since the shock elasticity function depends on \(x_1\), the code computes percentiles of the shock elasticity based on the stationary distribution of \(x_1\). This is done by the internal function _compute_percentile in exposure_elasticity and price_elasticity.

def exposure_elasticity(log_M_growth, X1_tp1, X2_tp1, T=400, shock=0, percentile=0.5):

r"""

Computes exposure elasticity for M.

Parameters

----------

log_M_growth : LinQuadVar

Log growth of multiplicative functional M.

e.g. log consumption growth, :math:`\log \frac{C_{t+1}}{C_t}`

X1_tp1 : LinQuadVar

Stores the coefficients of laws of motion for X1.

X2_tp1 : LinQuadVar

Stores the coefficients of laws of motion for X2.

T : int

Time horizon.

shock : int

Position of the initial shock, starting from 0.

percentile : float

Specifies the percentile of the elasticities.

Returns

-------

elasticities : (T, n_Y) ndarray

Exposure elasticities.

Reference

---------

Borovicka, Hansen (2014). See http://larspeterhansen.org/.

"""

n_Y, n_X, n_W = log_M_growth.shape

if n_Y != 1:

raise ValueError("The dimension of input should be 1.")

α = np.zeros(n_W)

α[shock] = 1

p = norm.ppf(percentile)

Σ_tilde_t, μ_t0, μ_t1 = _elasticity_coeff(log_M_growth, X1_tp1, X2_tp1, T)

kron_product = np.kron(X1_tp1['x'], X1_tp1['x'])

x_mean = np.linalg.solve(np.eye(n_X)-X1_tp1['x'],X1_tp1['c'])

x_cov = mat(np.linalg.solve(np.eye(n_X**2)-kron_product,

vec(X1_tp1['w']@X1_tp1['w'].T)), (n_X, n_X))

elasticities = _exposure_elasticity_loop(T, n_Y, α, Σ_tilde_t, μ_t0,

μ_t1, percentile, x_mean, x_cov, p)

return elasticities

@njit(parallel=True)

def _exposure_elasticity_loop(T, n_Y, α, Σ_tilde_t, μ_t0, μ_t1, percentile, x_mean, x_cov, p):

elasticities = np.zeros((T, n_Y))

if percentile == 0.5:

for t in prange(T):

elasticity = (α@Σ_tilde_t[t]@μ_t0[t])[0] +(α@Σ_tilde_t[t]@μ_t1[t]@x_mean)[0]

elasticities[t] = elasticity

else:

for t in prange(T):

elasticity = (α@Σ_tilde_t[t]@μ_t0[t])[0] +(α@Σ_tilde_t[t]@μ_t1[t]@x_mean)[0]

A = α@Σ_tilde_t[t]@μ_t1[t]

elasticity = _compute_percentile(A, elasticity, x_cov, p)

elasticities[t] = elasticity

return elasticities

def price_elasticity(log_G_growth, log_S_growth, X1_tp1, X2_tp1, T=400, shock=0, percentile=0.5):

r"""

Computes price elasticity.

Parameters

----------

log_G_growth : LinQuadVar

Log growth of multiplicative functional G.

e.g. log consumption growth, :math:`\log \frac{C_{t+1}}{C_t}`

log_S_growth : LinQuadVar

Log growth of multiplicative functional S.

e.g. log stochastic discount factor, :math:`\log \frac{S_{t+1}}{S_t}`

X1_tp1 : LinQuadVar

Stores the coefficients of laws of motion for X1.

X2_tp2 : LinQuadVar or None

Stores the coefficients of laws of motion for X2.

T : int

Time horizon.

shock : int

Position of the initial shock, starting from 0.

percentile : float

Specifies the percentile of the elasticities.

Returns

-------

elasticities : (T, dim) ndarray

Price elasticities.

Reference

---------

Borovicka, Hansen (2014). See http://larspeterhansen.org/.

"""

if log_G_growth.shape != log_S_growth.shape:

raise ValueError("The dimensions of G and S do not match.")

else:

n_Y, n_X, n_W = log_G_growth.shape

if n_Y != 1:

raise ValueError("The dimension of inputs should be (1, n_X, n_W)")

α = np.zeros(n_W)

α[shock] = 1

p = norm.ppf(percentile)

Σ_tilde_expo_t, μ_expo_t0, μ_expo_t1 \

= _elasticity_coeff(log_G_growth, X1_tp1, X2_tp1, T)

Σ_tilde_value_t, μ_value_t0, μ_value_t1\

= _elasticity_coeff(log_G_growth+log_S_growth, X1_tp1, X2_tp1, T)

kron_product = np.kron(X1_tp1['x'], X1_tp1['x'])

x_mean = np.linalg.solve(np.eye(n_X)-X1_tp1['x'],X1_tp1['c'])

x_cov = mat(np.linalg.solve(np.eye(n_X**2)-kron_product,

vec(X1_tp1['w']@X1_tp1['w'].T)), (n_X, n_X))

elasticities = _price_elasticity_loop(T, n_Y, α, Σ_tilde_expo_t, Σ_tilde_value_t,

μ_expo_t0, μ_value_t0, μ_expo_t1, μ_value_t1,

percentile, x_mean, x_cov, p)

return elasticities

@njit(parallel=True)

def _price_elasticity_loop(T, n_Y, α, Σ_tilde_expo_t, Σ_tilde_value_t,

μ_expo_t0, μ_value_t0, μ_expo_t1, μ_value_t1,

percentile, x_mean, x_cov, p):

elasticities = np.zeros((T, n_Y))

if percentile == 0.5:

for t in prange(T):

elasticity = (α @ (Σ_tilde_expo_t[t] @ μ_expo_t0[t] \

- Σ_tilde_value_t[t] @ μ_value_t0[t]))[0]\

+(α@(Σ_tilde_expo_t[t]@μ_expo_t1[t]@x_mean\

- Σ_tilde_value_t[t] @ μ_value_t1[t]@x_mean))[0]

elasticities[t] = elasticity

else:

for t in prange(T):

elasticity = (α @ (Σ_tilde_expo_t[t] @ μ_expo_t0[t]\

- Σ_tilde_value_t[t] @ μ_value_t0[t]))[0]\

+(α@(Σ_tilde_expo_t[t]@μ_expo_t1[t]@x_mean\

- Σ_tilde_value_t[t] @ μ_value_t1[t]@x_mean))[0]

A = α @ (Σ_tilde_expo_t[t]@μ_expo_t1[t]\

- Σ_tilde_value_t[t]@μ_value_t1[t])

elasticity = _compute_percentile(A, elasticity, x_cov, p)

elasticities[t] = elasticity

return elasticities

@njit

def _compute_percentile(A, Ax_mean, x_cov, p):

r"""

Compute percentile of the scalar Ax, where A is vector coefficient and x follows multivariate normal distribution.

Parameters

----------

A : (N, ) ndarray

Coefficient of Ax.

Ax_mean : float

Mean of Ax.

x_cov : (N, N) ndarray

Covariance matrix of x.

p : float

Percentile of a standard normal distribution.

Returns

-------

res : float

Percentile of Ax.

"""

Ax_var = A@x_cov@A.T

Ax_std = np.sqrt(Ax_var)

res = Ax_mean + Ax_std * p

return res

3. An Illustration using the Long-Run Risk Model [1]#

This example uses the long-run risk model numerical results in the exponential-linear–quadratic framework to calculate shock elasticities. The variables are expressed in Python LinQuadVar objects, which store the coefficients in linear-quadratic structure. The LinQuadVar allows the add and multiply operations. Using coefficients from [1], we form the approximation:

and the log consumption is approximately

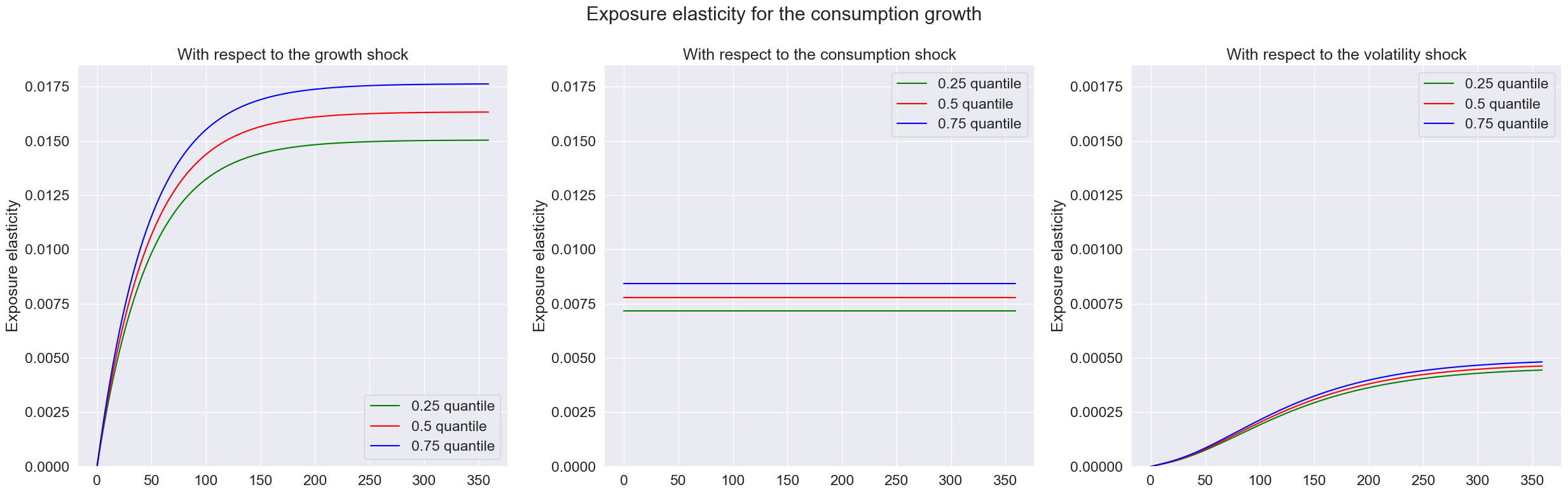

3.1 Exposure Elasticity for Consumption Growth#

To calculate the exposure elasticity for consumption growth using the exposure_elasticity defined above, we need six inputs

Consumption growth, gc_tp1, loaded from outside solutions. This is a LinQuadVar object.

First order expansion of the state evolution equations, X1_tp1, loaded from outside solutions. This is a LinQuadVar object.

Second order expansion of the state evolution equations, X2_tp1, loaded from outside solutions. This is a LinQuadVar object.

Time periods, \(\text{T} = 360\), 30 years

Shock index, \(0\) stands for the growth shock, which means \(\alpha' =\begin{bmatrix}1 & 0 & 0 & 0 \end{bmatrix}\), \(1\) stands for the volatility shock, \(2\) stands for the consumption shock. The fourth shock alters dividend growth and its shock prices are zero.

Percentile, \(0.5\) stands for the median

import pickle

import matplotlib.pyplot as plt

import seaborn as sns

import pandas as pd

pd.options.display.float_format = '{:.3g}'.format

sns.set(font_scale = 1.5)

"""

load the long-run risk model solutions when ρ = 2/3, 1, 1.5, 10

"""

with open(workdir + '/data/res_006.pkl', 'rb') as f:

res_006 = pickle.load(f)

with open(workdir + '/data/res_010.pkl', 'rb') as f:

res_010 = pickle.load(f)

with open(workdir + '/data/res_015.pkl', 'rb') as f:

res_015 = pickle.load(f)

with open(workdir + '/data/res_100.pkl', 'rb') as f:

res_100 = pickle.load(f)

# Compute the shock elasticity for 30 years

T = 360

# Calculate the shock elasticity at 0.25, 0.5 and 0.75 quantile

quantile = [0.25, 0.5, 0.75]

# Load the consumption and state evolution process

gc_tp1 = res_015['gc_tp1']

X1_tp1 = res_015['X1_tp1']

X2_tp1 = res_015['X2_tp1']

## Calculate exposure elasticity for consumption growth

expo_elas_shock_0_015 = [exposure_elasticity(gc_tp1, X1_tp1, X2_tp1, T, shock=0, percentile=p) for p in quantile] # The first shock is the growth shock

expo_elas_shock_1_015 = [exposure_elasticity(gc_tp1, X1_tp1, X2_tp1, T, shock=1, percentile=p) for p in quantile] # The second shock is the volatility shock

expo_elas_shock_2_015 = [exposure_elasticity(gc_tp1, X1_tp1, X2_tp1, T, shock=2, percentile=p) for p in quantile] # The third shock is the consumption shock

## Plot the exposure elasticity for consumption growth

index = ['T','0.25 quantile','0.5 quantile','0.75 quantile']

fig, axes = plt.subplots(1,3, figsize = (25,8))

expo_elas_shock_0 = pd.DataFrame([np.arange(T),expo_elas_shock_0_015[0].flatten(),expo_elas_shock_0_015[1].flatten(),expo_elas_shock_0_015[2].flatten()], index = index).T

expo_elas_shock_1 = pd.DataFrame([np.arange(T),expo_elas_shock_1_015[0].flatten(),expo_elas_shock_1_015[1].flatten(),expo_elas_shock_1_015[2].flatten()], index = index).T

expo_elas_shock_2 = pd.DataFrame([np.arange(T),expo_elas_shock_2_015[0].flatten(),expo_elas_shock_2_015[1].flatten(),expo_elas_shock_2_015[2].flatten()], index = index).T

n_qt = len(quantile)

plot_elas = [expo_elas_shock_0, expo_elas_shock_2, expo_elas_shock_1] # For illustration purpose, the consumption shock is plotted in the second column, the volatility shock is plotted in the third column

shock_name = ['growth shock', 'consumption shock', 'volatility shock']

qt = ['0.25 quantile','0.5 quantile','0.75 quantile']

colors = ['green','red','blue']

for i in range(len(plot_elas)):

for j in range(n_qt):

sns.lineplot(data = plot_elas[i], x = 'T', y = qt[j], ax=axes[i], color = colors[j], label = qt[j])

axes[i].set_xlabel('')

axes[i].set_ylabel('Exposure elasticity')

axes[i].set_title('With respect to the ' + shock_name[i])

axes[2].set_ylim([0,0.00185])

axes[1].set_ylim([0,0.0185])

axes[0].set_ylim([0,0.0185])

fig.suptitle('Exposure elasticity for the consumption growth')

fig.tight_layout()

plt.show()

## Calculate exposure elasticity for consumption growth at the limit

log_f = LinQuadVar({'c': np.zeros((1,1))},gc_tp1.shape)

Qf_components_log_C, _, η_C, η_C_series = Q_mapping(gc_tp1, log_f, X1_tp1, X2_tp1, tol = 1e-7)

expo_elas_shock_0_015_limit = [exposure_elasticity(gc_tp1, X1_tp1, X2_tp1, len(η_C_series), shock=0, percentile=p)[-1].item() for p in quantile]

expo_elas_shock_1_015_limit = [exposure_elasticity(gc_tp1, X1_tp1, X2_tp1, len(η_C_series), shock=1, percentile=p)[-1].item() for p in quantile]

expo_elas_shock_2_015_limit = [exposure_elasticity(gc_tp1, X1_tp1, X2_tp1, len(η_C_series), shock=2, percentile=p)[-1].item() for p in quantile]

expo_limit = pd.DataFrame([expo_elas_shock_0_015_limit, expo_elas_shock_2_015_limit,expo_elas_shock_1_015_limit],\

columns = ['0.25 quantile','0.5 quantile','0.75 quantile'],\

index = ['Growth Shock','Consumption Shock','Volatility Shock']).T

expo_limit

| Growth Shock | Consumption Shock | Volatility Shock | |

|---|---|---|---|

| 0.25 quantile | 0.015 | 0.00718 | 0.000458 |

| 0.5 quantile | 0.0163 | 0.0078 | 0.000477 |

| 0.75 quantile | 0.0176 | 0.00842 | 0.000496 |

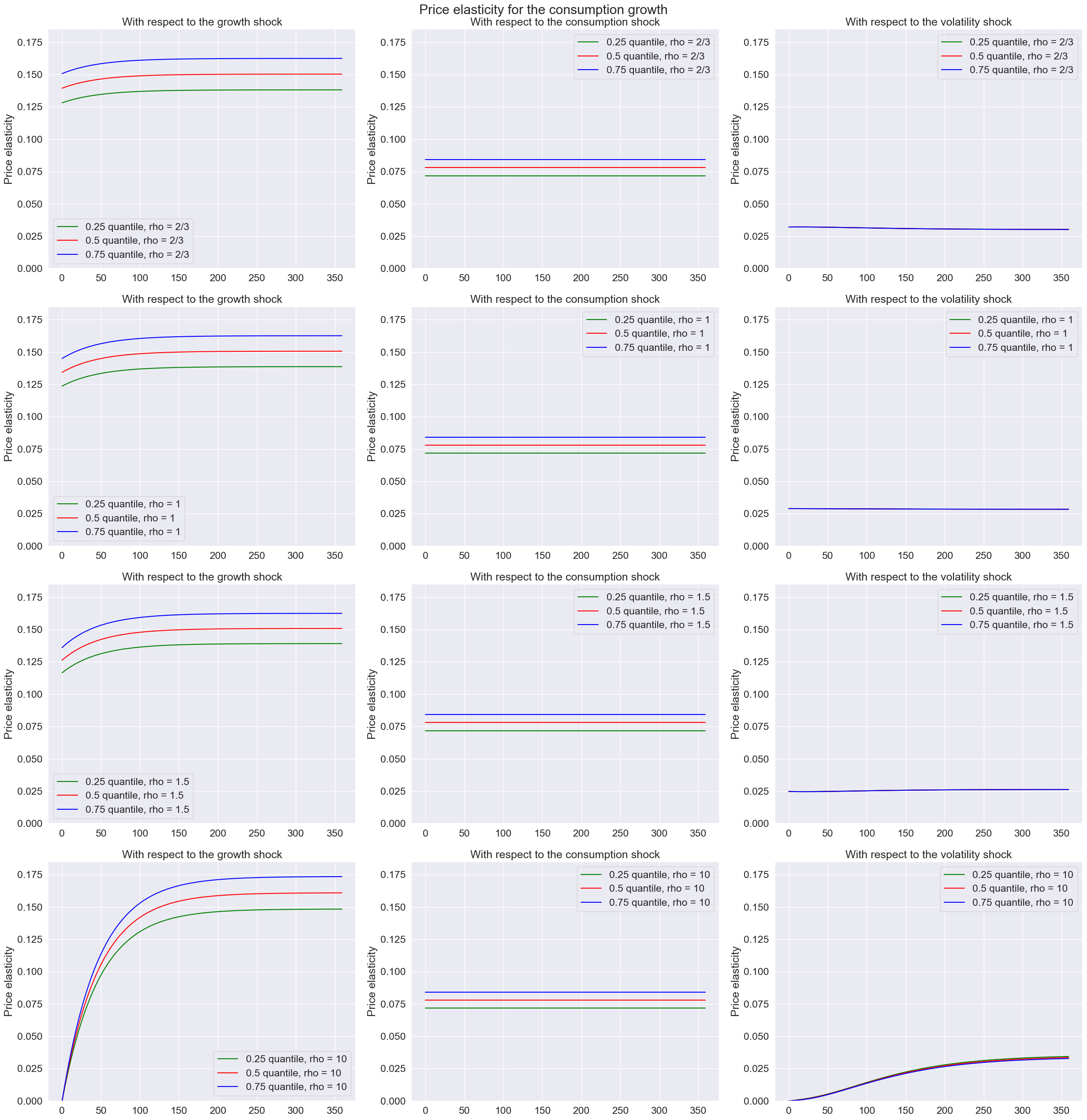

3.2 Calculate Price Elasticity for Consumption Growth#

Similarly, to calculate the price elasticity for consumption growth using the price_elasticity defined above, we need additional inputs

Log Stochastic Discount Factor

We construct the log SDF using equation (7), then input it into the function to calculate price elasticity. The code uses the following formula for the log SDF:

where

and \(\left(\widehat{V}_{t+1}-\widehat{R}_t\right)\) is the logarithm of the risk adjustment continuation value. The random variable \(N_{t+1}^*\) is positive and has expectation one conditioned on date \(t\) information. It implies a substantively interesting change in the probablity measure.

We approximate the term \(\frac{1}{1-\gamma}\log N_{t+1}^*\) differently than the \(\left(\widehat{V}_{t+1}-\widehat{R}_t\right)\) in the \((\rho-1)\left(\widehat{V}_{t+1}-\widehat{R}_t\right)\) term. We use an approximation of the former term that ensures \(N_{t+1}^*\) is positive and has conditional expectation one.

def calc_SDF(res):

r'''

This function loads external results for the long-run risk model with different rho values, and then calculates the SDF.

Parameters

----------

res : dictionary of LinQuadVar

Stores the external solution for the long-run risk model

Returns

-------

log_SDF : LinQuadVar

Stores coefficients of the log SDF

gc_tp1 : LinQuadVar

Stores the coefficients of the consumption growth process.

X1_tp1 : LinQuadVar

Stores the coefficients of the first order expansion of the state evolution equations.

X2_tp1 : LinQuadVar

Stores the coefficients of the second order expansion of the state evolution equations.

'''

n_J, n_X, n_W = res['var_shape']

β = res['β']

ρ = res['ρ']

X1_tp1 = res['X1_tp1']

X2_tp1 = res['X2_tp1']

gc_tp1 = res['gc_tp1']

gc0_tp1 = res['gc0_tp1']

gc1_tp1 = res['gc1_tp1']

gc2_tp1 = res['gc2_tp1']

vmr1_tp1 = res['vmr1_tp1']

vmr2_tp1 = res['vmr2_tp1']

log_N_tilde = res['log_N_tilde']

S0_tp1 = LinQuadVar({'c':np.log(β) - ρ*np.array([[gc0_tp1]])}, shape = (1,n_X,n_W))

S1_tp1 = (ρ-1)*vmr1_tp1 -ρ*gc1_tp1

S2_tp1 = (ρ-1)*vmr2_tp1 -ρ*gc2_tp1

log_SDF = S0_tp1 + S1_tp1 + 0.5 *S2_tp1 + log_N_tilde

return log_SDF, gc_tp1, X1_tp1, X2_tp1

## Calculate the log SDF when ρ = 2/3

log_SDF, gc_tp1, X1_tp1, X2_tp1 = calc_SDF(res_006)

## Calculate price elasticity for consumption growth when ρ = 2/3

price_elas_shock_0_006 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=0, percentile=p) for p in quantile]

price_elas_shock_1_006 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=1, percentile=p) for p in quantile]

price_elas_shock_2_006 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=2, percentile=p) for p in quantile]

## Calculate the log SDF when ρ = 1

log_SDF, gc_tp1, X1_tp1, X2_tp1 = calc_SDF(res_010)

## Calculate price elasticity for consumption growth when ρ = 1

price_elas_shock_0_010 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=0, percentile=p) for p in quantile]

price_elas_shock_1_010 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=1, percentile=p) for p in quantile]

price_elas_shock_2_010 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=2, percentile=p) for p in quantile]

## Calculate the log SDF when ρ = 1.5

log_SDF, gc_tp1, X1_tp1, X2_tp1 = calc_SDF(res_015)

## Calculate price elasticity for consumption growth when ρ = 1.5

price_elas_shock_0_015 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=0, percentile=p) for p in quantile]

price_elas_shock_1_015 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=1, percentile=p) for p in quantile]

price_elas_shock_2_015 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=2, percentile=p) for p in quantile]

## Calculate the log SDF when ρ = 10

log_SDF, gc_tp1, X1_tp1, X2_tp1 = calc_SDF(res_100)

## Calculate price elasticity for consumption growth when ρ = 10

price_elas_shock_0_100 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=0, percentile=p) for p in quantile]

price_elas_shock_1_100 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=1, percentile=p) for p in quantile]

price_elas_shock_2_100 = [price_elasticity(gc_tp1, log_SDF, X1_tp1, X2_tp1, T, shock=2, percentile=p) for p in quantile]

## Plot the price elasticity for consumption growth

fig, axes = plt.subplots(4,3, figsize = (25,26))

index = ['T','rho 006 0.25 quantile','rho 006 0.5 quantile','rho 006 0.75 quantile','rho 010 0.25 quantile','rho 010 0.5 quantile','rho 010 0.75 quantile',\

'rho 015 0.25 quantile','rho 015 0.5 quantile','rho 015 0.75 quantile','rho 100 0.25 quantile','rho 100 0.5 quantile','rho 100 0.75 quantile']

price_elas_shock_0 = pd.DataFrame([np.arange(T),price_elas_shock_0_006[0].flatten(),price_elas_shock_0_006[1].flatten(),price_elas_shock_0_006[2].flatten(),\

price_elas_shock_0_010[0].flatten(),price_elas_shock_0_010[1].flatten(),price_elas_shock_0_010[2].flatten(),\

price_elas_shock_0_015[0].flatten(),price_elas_shock_0_015[1].flatten(),price_elas_shock_0_015[2].flatten(),\

price_elas_shock_0_100[0].flatten(),price_elas_shock_0_100[1].flatten(),price_elas_shock_0_100[2].flatten()],index = index).T

price_elas_shock_1 = pd.DataFrame([np.arange(T),-price_elas_shock_1_006[0].flatten(),-price_elas_shock_1_006[1].flatten(),-price_elas_shock_1_006[2].flatten(),\

-price_elas_shock_1_010[0].flatten(),-price_elas_shock_1_010[1].flatten(),-price_elas_shock_1_010[2].flatten(),\

-price_elas_shock_1_015[0].flatten(),-price_elas_shock_1_015[1].flatten(),-price_elas_shock_1_015[2].flatten(),\

-price_elas_shock_1_100[0].flatten(),-price_elas_shock_1_100[1].flatten(),-price_elas_shock_1_100[2].flatten()],index = index).T

price_elas_shock_2 = pd.DataFrame([np.arange(T),price_elas_shock_2_006[0].flatten(),price_elas_shock_2_006[1].flatten(),price_elas_shock_2_006[2].flatten(),\

price_elas_shock_2_010[0].flatten(),price_elas_shock_2_010[1].flatten(),price_elas_shock_2_010[2].flatten(),\

price_elas_shock_2_015[0].flatten(),price_elas_shock_2_015[1].flatten(),price_elas_shock_2_015[2].flatten(),\

price_elas_shock_2_100[0].flatten(),price_elas_shock_2_100[1].flatten(),price_elas_shock_2_100[2].flatten()],index = index).T

n_rho = 4

n_qt = len(quantile)

plot_elas = [price_elas_shock_0,price_elas_shock_2,price_elas_shock_1]

shock_name = ['growth shock', 'consumption shock', 'volatility shock']

rho_y = ['rho 006', 'rho 010', 'rho 015', 'rho 100']

rho_label = ['rho = 2/3','rho = 1','rho = 1.5','rho = 10']

qt = ['0.25 quantile','0.5 quantile','0.75 quantile']

colors = ['green','red','blue']

for k in range(len(plot_elas)):

for i in range(n_rho):

for j in range(n_qt):

sns.lineplot(data = plot_elas[k], x = 'T', y = rho_y[i] +' ' + qt[j], ax=axes[i,k], color = colors[j], label = qt[j]+', '+rho_label[i])

axes[i,k].set_xlabel('')

axes[i,k].set_ylabel('Price elasticity')

axes[i,k].set_ylim([0,0.185])

axes[i,k].set_title('With respect to the '+ shock_name[k])

fig.suptitle('Price elasticity for the consumption growth')

fig.tight_layout()

plt.show()

3.3 Shock Elasticities under Different Parameter Settings#

Below is a brief UI to select parameters shown in the long-run risk model [1]. The stochastic volatility process has been normalized with its mean equal to 1. By changing the inputs of parameters, we can see how shock elasticities vary with respect to these parameters.

from ipywidgets import interact

from BY_example_sol import solve_BY_elas

interact(solve_BY_elas, γ=[('5',5), ('10',10),('15',15),('20',20)],\

β=[('0.995',0.995),('0.998',0.998), ('0.999',0.999)],\

ρ=[('2/3', 2./3),('1', 1.0001),('1.5', 1.5),('10', 10)],\

α=[('0.969',0.969),('0.979',0.979),('0.989',0.989)],\

ϕ_e=[('0.0002',0.0002),('0.0003432',0.0003432),('0.0004',0.0004)],\

ν_1=[('0.977',0.977),('0.987',0.987),('0.997',0.997)],\

σ_w=[('0.03',0.03),('0.0378',0.0378),('0.04',0.04)],\

μ=[('0.0005', 0.0005),('0.0015', 0.0015),('0.003',0.003)],\

ϕ_c=[('0.002',0.002),('0.0078',0.0078),('0.01',0.01)]);

Iteration 1: error = 9.93379444

Iteration 2: error = 0

Current paramter settings

γ = 10

β = 0.998

ρ = 0.6667

α = 0.979

ϕ_e = 0.0002

ν_1 = 0.987

σ_w = 0.03

μ = 0.0015

ϕ_c = 0.0078

Reference#

[1] Bansal, Ravi, and Amir Yaron. “Risks for the long run: A potential resolution of asset pricing puzzles.” The journal of Finance 59, no. 4 (2004): 1481-1509.

[2] Borovička, Jaroslav, and Lars Peter Hansen. “Term structure of uncertainty in the macroeconomy.” In Handbook of Macroeconomics, vol. 2, pp. 1641-1696. Elsevier, 2016.

[3] Borovička, Jaroslav, and Lars Peter Hansen. “Examining macroeconomic models through the lens of asset pricing.” Journal of Econometrics 183, no. 1 (2014): 67-90.

[4] Lombardo, Giovanni, and Harald Uhlig. “A theory of pruning.” International Economic Review 59, no. 4 (2018): 1825-1836.