![]()

4 Heterogeneous Agents#

This Python notebook covers the environment in section 5. We need to solve the following:

Expert’s HJB equation

Household’s HJB equation

Optimal expert capital share

Optimal expert equity retention

Where:

Since \(\chi\) can be solved algebraically, we solve (1) to (3).

4.1 Solution Overview#

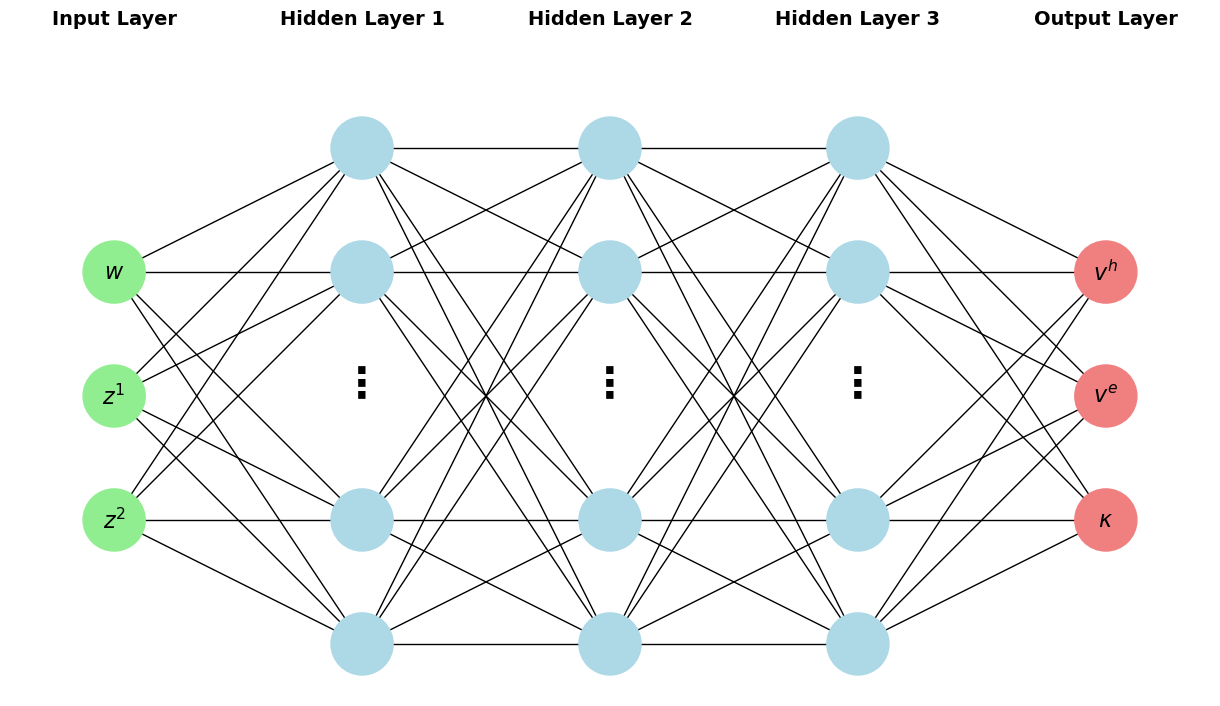

4.1.1 Model Architecture#

We modify the DeepGalerkinMethod code from the companion code to Correia et. al 2018. We construct a feedforward, fully-connected neural network to approximate \(v^e\), \(v^h\) and \(\kappa\) as functions of the states.

Fig. 2 Neural network architecture used in this computation. Note that in the paper, layer_width=16.#

We employ the following hyperparameters:

Input |

Description |

Parameter used in paper |

|---|---|---|

|

Number of layers |

2 |

|

Number of neurons in each layer |

16 |

|

Dimension of input into first layer |

3 (This should be the same as the number of states) |

|

Activation function for all layers except the last |

tanh |

|

Activation function for final layer |

Identity function for first two dimensions; sigmoid for third dimension. This is so that… |

|

Seed for weight and bias initialization |

256 |

We use a Glorot normal initializer to initialize weights and a Glorot uniform initializer to initialize the biases.

4.1.2 Training#

The training set is constructed by drawing uniformly from the three-dimensional cube bounded by [wMin,zMin,vMin] and [wMax,zMax,vMax]. The loss function is given by the mean squared error of \(L\), where:

Where \(p\) is a penalization parameter. We compute gradients using tf.GradientTape and use an L-BFGS-B solver. For the settings used in the paper, there are 659 trainable variables: 3x16 weights and 16 bias terms for the initial layer; 16x16 weights and 16 bias terms for each hidden layer; and 16x3 weights and 3 bias terms for the final layer. The full list of parameters for the training stage are:

Input |

Description |

Parameter used in paper |

|---|---|---|

|

Determines the |

10 |

|

Number of epochs, i.e. the number of complete passes through the training set |

5 |

|

Penalty for violating \(\kappa\) constraint |

10000 |

|

Seed for drawing uniform samples |

256 (same as seed for initialization) |

|

Maximum number of L-BFGS-B iterations (number of times parameters are updated) per epoch |

100 |

|

Maximum number of function evaluations per epoch |

100 |

|

The maximum number of variable metric corrections used to define the limited memory matrix used to compute the Hessian per epoch |

100 |

|

Maximum number of line search steps per iteration used to find the optimal step-size |

100 |

|

Iteration will stop when \(\max|proj(g_i)| \leq\) |

Machine epsilon for float64 (~\(2^{-16}\)) |

|

Iteration will stop when \(\frac{L^k - L^{k+1}}{\max{|L^k|,|L^{k+1}|,1}} \leq\) |

Machine epsilon for float64 (~\(2^{-16}\)) |

|

Iteration will stop when, after fully completing an epoch, \(L\) is less than |

\(10^{-5}\) |

4.1.3 Model Parameters#

We also need to set model parameters. These will vary depending on the environment chosen from Section 5.1. By default, the following parameters are allowed as inputs to main_BFGS:

Input |

Description |

Parameter used in paper |

|---|---|---|

|

Skin-in-the-game constraint |

\(\underline{\chi}\) |

|

Expert and household uncertainty aversion |

\(\gamma_e, \gamma_h\) |

|

Expert and household productivity |

\(\alpha_e, \alpha_h\) |

|

Expert and household discount rate |

\(\delta_e, \delta_h\) |

|

Expert and household inverse of IES |

\(\rho_e, \rho_h\) |

|

Birth/death rate |

\(\lambda_d\) |

|

Fraction of newborns which are experts |

\(\nu\) |

|

Mean of \(Z_2\) |

\(\mu_2\) |

|

Normalization for variances; these are multiplied by the covariance matrix specified in |

|

|

Bounds for training set for \(W\); the corresponding bounds for \(Z_1\) and \(Z_2\) can be edited in |

|

|

Number of gridpoints for each state variable; this does not have any effect on the solution but will determine the evaluation of variables of interest using the solution at a later step |

|

|

Determines whether the shock exposure matrix is “upper_triangular” or “lower_triangular” |

In addition, the following parameters can be edited in the utils_para file. They do not vary across the models explored in the paper, but the user may wish to explore their own variations.

Input |

Description |

Notation used in paper |

Default used in paper |

|---|---|---|---|

|

Mean of \(Z^1\) |

0.0 |

|

|

Persistence of $Z^1 |

\(\beta_1\) |

0.056 |

|

Persistence of \(Z^2\) |

\(\beta_2\) |

0.194 |

|

\(\eta_k\) |

\(\alpha\) |

0.04 |

|

Adjustment cost |

\(\phi\) |

8.0 |

|

\(i,j\) entry in shock exposure matrix |

See Table 1 in paper |

|

|

Governs grid size for \(Z^1\) and \(Z^2\) (number of standard deviations from the mean) |

5 |

|

|

Grid boundaries for \(Z^1\) |

\(\mu_1 \pm SD\cdot Var(Z_1|Z_2=\mu_2)\) where \(SD=\) |

|

|

Grid boundaries for \(Z^2\) |

|

4.2 Quick Start#

We can build and train the neural network as follows. First, we import libraries:

import json

import numpy as np

import tensorflow as tf

import time

import os

os.chdir("src/4")

from main_BFGS import main

from utils_para import setModelParameters

from utils_training import training_step_BFGS

from utils_DGM import DGMNet

os.chdir("../..")

import warnings

warnings.filterwarnings("ignore")

tf.get_logger().setLevel('ERROR')

tf.config.set_visible_devices([], 'GPU')

Next, we set the model parameters and hyperparameters. In the following example, we have used a variant of Model RF.

chiUnderline = 1.0

gamma_e = 4.0

a_e=0.0922

a_h=0.0

gamma_h=4.0

delta_e=0.0115

delta_h=0.01

lambda_d=0.0

rho_e=1.0

rho_h=1.0

nu=0.1

V_bar=0.0000063030303030303026

sigma_K_norm=3.1707442821755683

sigma_Z_norm=19.835431735873996

sigma_V_norm=0.0010882177801089308

wMin=0.01

wMax=0.99

nWealth=180

nZ=30

nV=30

seed_=(256)

n_layers_=(2)

units_=(16)

points_size_=(10)

iter_num_=(5)

penalization=10000

BFGSmaxiter=100

BFGSmaxfun=100

action_name = 'test'

seed=256

n_layers=2

units=16

points_size=10

iter_num=5

penalization=10000

BFGS_maxiter=100

BFGS_maxfun=100

shock_expo = 'upper_triangular'

Next, we run the main solution, which trains the neural network. Under the parameterization above, this will take around 1 minute.

main(action_name, nWealth, nZ, nV, V_bar, sigma_K_norm, sigma_Z_norm, sigma_V_norm, wMin, wMax, chiUnderline, a_e, a_h, gamma_e, gamma_h, rho_e, rho_h, delta_e, delta_h, lambda_d, nu, shock_expo, n_layers, points_size, iter_num, units, seed, penalization, BFGS_maxiter, BFGS_maxfun)

Now that we have a solution, we can compute variables of interest, which can subsequently be used to compute shock elasticities. By default, main_variable computes the following variables. Unless specified otherwise, the variables are evaluated on an array with dimension [nWealth,nZ,nV].

Output |

Description |

Notation used in paper |

|---|---|---|

|

The values of \(W\), \(Z_1\) and \(Z_2\) on the state-space grid |

|

|

Expert and household value functions |

\(V_e\), \(V_h\) |

|

Log expert and household value functions |

\(\hat{V}_e\), \(\hat{V}_h\) |

|

Expert equity retention |

\(\chi\) |

|

Expert capital share |

\(\kappa\) |

|

Risk-free rate |

\(r\) |

|

Price of capital |

\(Q\) |

|

State volatilities |

\(Z^2 \sigma_w\),\(Z^2 \sigma_1\), \(Z^2 \sigma_2\) |

|

State drifts |

\(\mu_w\),\(\mu_1\),\(\mu_2\) |

|

Log capital drift |

\(\mu_{k}\) |

|

Log capital diffusin |

\(\sigma_{k}\) |

|

Capital price drift |

\(\mu_q\) |

|

Capital price diffusion |

\(\sigma_q\) |

|

Capital return volatility |

\(\sigma_r\) |

|

Expert and household risk premium wedge |

\(\Delta^e\),\(\Delta^h\) |

|

Expert and household equity risk price |

\(\pi_e\),\(\pi_h\) |

|

\(\frac{\chi \kappa}{W}\), \(\frac{1- \kappa}{W}\) |

|

|

RHS of HJB equations and \(\kappa\) constraint evaluated on the state space grid |

\(L^e\), \(L^h\), \(L^{\kappa}\) |

|

Loss function (scalar) |

|

|

Stationary density |

|

|

First and second derivatives of expert and household value function with respect to each of the states; separate objects for each state are also included |

|

|

Log SDF drifts for expert and household |

\(-r_t S_t^e\), \(-r_t S_t^h\) |

|

Log SDF diffusions for expert and household |

\(-S_t^e \pi_t^e\), \(-S_t^h \pi_t^h\) |

|

Log consumption drifts for expert and household |

\(\hat{\mu}_c^e\), \(\hat{\mu}_c^h\) |

|

Log consumption diffusions for expert and household |

\(\sigma_c^e\), \(\sigma_c^h\) |

|

Log aggregate consumption drift |

\(\hat{\mu}_c\) |

|

Log aggregate consumption diffusion |

\(\sigma_c\) |

Given that a solution has been saved under the same parameters, the following code outputs the variables listed above. In addition, the marginal_quantile_func_factory function is called to save the above outputs evaluated at desired quantiles (e.g. \(Z^2\) at median) for ease of plotting.

os.chdir('src/4')

from main_variable import main_var

os.chdir('../..')

main_var(action_name, nWealth, nZ, nV, V_bar, sigma_K_norm, sigma_Z_norm, sigma_V_norm, wMin, wMax, chiUnderline, a_e, a_h, gamma_e, gamma_h, rho_e, rho_h, delta_e, delta_h, lambda_d, nu, shock_expo, n_layers, units, points_size, iter_num, seed, penalization, BFGS_maxiter, BFGS_maxfun)

2024-09-03 01:55:37.533890: I tensorflow/core/platform/cpu_feature_guard.cc:193] This TensorFlow binary is optimized with oneAPI Deep Neural Network Library (oneDNN) to use the following CPU instructions in performance-critical operations: AVX2 AVX512F AVX512_VNNI FMA

To enable them in other operations, rebuild TensorFlow with the appropriate compiler flags.

4.3 Plotting#

We can now plot the results.

import os

import numpy as np

os.chdir('src/4')

from plot import return_NN_solution

os.chdir('../..')

import matplotlib.pyplot as plt

import seaborn as sns

sns.set(style="whitegrid", font_scale=1.13, rc={"lines.linewidth": 3.5})

plt.rcParams['axes.formatter.useoffset'] = True

First we load in the results using the same parameters as before.

results = return_NN_solution(shock_expo=shock_expo, seed=seed, chiUnderline=chiUnderline, a_e=a_e, a_h=a_h, gamma_e=gamma_e, gamma_h=gamma_h, psi_e=rho_e, psi_h=rho_h, delta_e=delta_e, delta_h=delta_h, lambda_d=lambda_d, nu=nu, n_layers=n_layers, units=units, iter_num=iter_num, points_size=points_size, penalization=penalization, action_name=action_name)

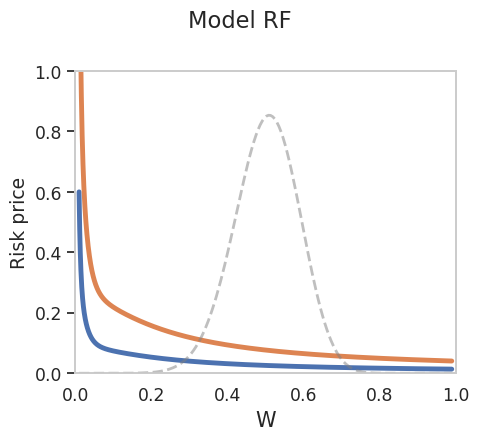

We provide an example plot below. Notice that we use results['eva_V_10'] and results['eva_V_90'] to extract the variables of interest evaluated at \(Z^1=0\) and \(Z^2\) at its 10th and 90th percentiles, respectively.

fig, ax = plt.subplots(1,1, figsize=(5,4.5))

W_dense = np.unique(results['eva_V_50']['W'])

W_sparse = np.unique(results['W'].values)

sns.lineplot(x = W_dense, y = results['eva_V_10']['PiE_NN'][:,0], ax = ax)

sns.lineplot(x = W_dense, y = results['eva_V_90']['PiE_NN'][:,0], ax = ax)

ax2 = ax.twinx()

sns.lineplot(x = W_sparse, y = results['dentW'].values, ax = ax2, ls='--', color='grey',lw=2.0, alpha=0.5)

ax2.grid(False)

ax2.set_yticks([])

ax2.set_ylim([0,0.03])

ax.set_xlim(0,1.0)

ax.grid(False)

ax.set_ylim([0.0,1.0])

ax.set_xlabel('W', fontsize=15)

ax.set_ylabel('Risk price')

plt.suptitle("Model RF")

plt.tight_layout()

4.4 Finite Difference Method#

We employ a finite differences method from mfrSuite to solve the two-dimensional Model IP from Section 5, which we cover briefly here.

import mfr.modelSoln as m

import numpy as np

import argparse

import os

import sys

import warnings

warnings.filterwarnings("ignore")

os.chdir('src/5')

from main_solve import main_fdm

from main_evaluate import interpolate

os.chdir('../..')

The model inputs are identical to the neural network solution above, except that: we abstract away from \(Z^2\); we have to set \(dt\), the false-transient time-step; and some inputs have been moved inside the main_solve.py script.

chiUnderline = 1.0

a_e=0.0922

a_h=0.085

gamma_e = 2.0

gamma_h= 2.0

delta_e=0.03

delta_h=0.01

lambda_d=0.0

rho_e=1.0

rho_h=1.0

nu=0.1

dt = 0.1

nWealth=180

nZ=30

shock_expo = 'upper_triangular'

action_name = 'test'

main_fdm(nW=nWealth, nZ=nZ, dt=dt, a_e=a_e, a_h=a_h, rho_e=rho_e, rho_h=rho_h, gamma_e=gamma_e, gamma_h=gamma_h, chiUnderline=chiUnderline, action_name=action_name, shock_expo=shock_expo, delta_e=delta_e, delta_h=delta_h, lambda_d=lambda_d, nu=nu)

Show code cell output

Program converged. Took 8089 iterations and 199.59 seconds. 2.49% of the time was spent on dealing with the linear systems.

Parameter Value

nu_newborn 0.1

lambda_d 0.0

lambda_Z 0.056

lambda_V 0.0

lambda_Vtilde 0.0

Z_bar 0.0

V_bar 1.0

Vtilde_bar 0.0

sigma_K_norm 0.008696916904073742

sigma_Z_norm 0.049798518005773194

sigma_V_norm 0.0

sigma_Vtilde_norm 0.0

nWealth 180

nZ 30

nV 0

nVtilde 0

nDims 2

delta_e 0.03

delta_h 0.01

a_e 0.0922

a_h 0.085

rho_e 1.0

rho_h 1.0

phi 8.0

gamma_e 2.0

gamma_h 2.0

equityIss 2

hhCap 1

chiUnderline 1.0

method 2

dt 0.1

dtInner 0.1

tol 1e-05

innerTol 1e-05

maxIters 500000

maxItersInner 500000

iparm_2 28

iparm_3 0

iparm_28 0

iparm_31 0

numSds 5

wMin 0.001

wMax 0.999

logW -1

folderName output/test/upper_triangular/dt_0.1/nW_180_nZ_30/chiUnderline_1.000/a_e_0.092_a_h_0.085/gamma_e_2.000_gamma_h_2.000/rho_e_1.000_rho_h_1.000/delta_e_0.030_delta_h_0.010/lambda_d_0.000_nu_0.100

overwrite Yes

verbatim -1

exportFreq 1000000

cov11 0.9153150324227657

cov12 0.4027386142660167

cov21 0.0

cov22 1.0

Exporting solution information: time used, convergence error, etc.

Exporting state variables.

==========================================

Exporting numerical results.

==========================================

(1): Exporting risk prices and interest rate: q, piH, piE, deltaE, deltaH, r, I.

------------------------------------------------

(2) Exporting drifts: muQ, muX, muK, muRe, muRh.

------------------------------------------------

(3) Exporting vols: sigmaQ, sigmaR, sigmaK.

------------------------------------------------

(4) Exporting value and policy functions: XiE, XiH, cHatE, cHatH, kappa, chi, betaE, betaH.

------------------------------------------------

(5) Exporting derivs: first, second, and cross derivs of XiE and XiH.

------------------------------------------------

(6) Exporting the rest: experts' leverage, sigmaC, sigmaCe, sigmaCh, sigmaSe, sigmaSh, simgaLogY, muC, muCe, muCh, muY, muSe, muSh.

------------------------------------------------

Exporting matrices' information

==========================================

(1) Exporting matrix coefficients

------------------------------------------------

(2) Exporting matrices and RHSs.

------------------------------------------------

Before we can plot any variables of interest, we need to interpolate on our state space grid. Here we interpolate risk prices linearly using scipy.interpolate.griddata.

interpolate(nW=nWealth, nZ=nZ, dt=dt, a_e=a_e, a_h=a_h, rho_e=rho_e, rho_h=rho_h, gamma_e=gamma_e, gamma_h=gamma_h, chiUnderline=chiUnderline, action_name=action_name, shock_expo=shock_expo, delta_e=delta_e, delta_h=delta_h, lambda_d=lambda_d, nu=nu)

Show code cell output

interpolating PiE_final_capital

interpolating kappa_final

Now we can load and plot our results:

import pandas as pd

import pickle

np.set_printoptions(suppress=True, linewidth=200)

import matplotlib.pyplot as plt

import seaborn as sns

sns.set(style="whitegrid", font_scale=1.13, rc={"lines.linewidth": 3.5})

plt.rcParams['axes.formatter.useoffset'] = True

os.chdir("src/5")

from plot import return_fdm_solution

os.chdir("../..")

fdm_result = return_fdm_solution(shock_expo=shock_expo, dt=dt, nW=nWealth, chiUnderline=chiUnderline, a_e=a_e, a_h=a_h, gamma_e=gamma_e, gamma_h=gamma_h, rho_e=rho_e, rho_h=rho_h, delta_e=delta_e, delta_h=delta_h, lambda_d=lambda_d, nu=nu, action_name=action_name, nZ=nZ)

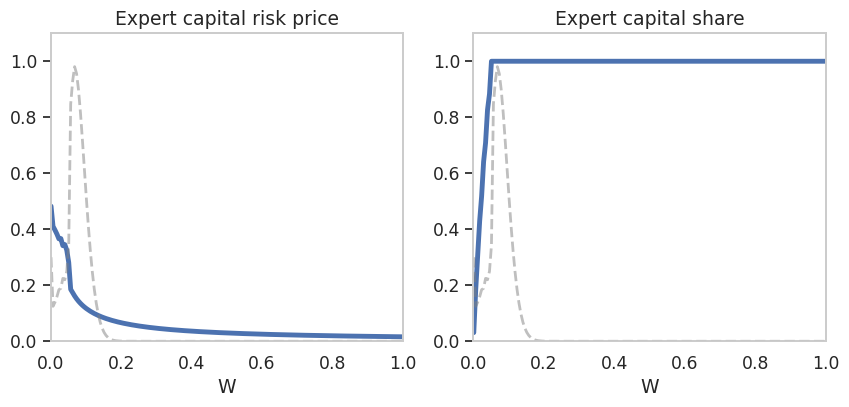

Here we plot the expert capital risk price and capital share as they vary with \(W\).

fig, axes = plt.subplots(1,2, figsize=(10,4))

W = fdm_result['W']['W'].unique()

sns.lineplot(x = W, y = fdm_result['PiE_final_capital'], ax = axes[0])

ax2 = axes[0].twinx()

sns.lineplot(x = W, y = fdm_result['dents'].values, ax = ax2, ls='--', color='grey',lw=2.0, alpha=0.5)

ax2.grid(False)

ax2.set_yticks([])

ax2.set_yticklabels([])

axes[0].set_ylim(0,1.1)

axes[0].set_xlim(0,1.0)

ax2.set_ylim([0,0.1])

axes[0].title.set_text("Expert capital risk price")

axes[0].set_xlabel('W')

sns.lineplot(x = W, y = fdm_result['kappa_final'], ax = axes[1])

ax2 = axes[1].twinx()

sns.lineplot(x = W, y = fdm_result['dents'].values, ax = ax2, ls='--', color='grey',lw=2.0, alpha=0.5)

ax2.grid(False)

ax2.set_yticks([])

ax2.set_yticklabels([])

axes[1].set_ylim(0,1.1)

axes[1].set_xlim(0,1.0)

ax2.set_ylim([0,0.1])

axes[1].title.set_text("Expert capital share")

axes[1].set_xlabel('W')

axes[0].grid(False)

axes[1].grid(False)